Why the Retroactive Date on Your Medmal Insurance Policy Matters

By Samantha Varela, Senior Legal Risk Advisor at Aon South Africa

Aon’s Legal Risk Management team is designed with an ethos aimed at simplifying sometimes seemingly complicated insurance concepts. The concept discussed in this article pertains to retroactive cover and claims made basis insurance cover.

Understanding the implications of the concept of what a retroactive date is, is a critical aspect of a medical malpractice claims-made insurance policy.

Its initial roots can be traced right back to the increased call for the introduction of a claims-made policy due to incidents involving long or indefinite periods of exposure, such as asbestos-related illnesses and severe pollution claims, the prevalence of which we saw rearing its head in the 1970s. These cases often took many years to manifest, patients presenting with symptoms of mesothelioma (a form of cancer which can be caused by exposure to asbestos) up to even 15 to 50 years after their asbestos exposure.

The introduction of the claims-made policy model sought to bring about clarity and an insurance solution to the often-murky determination of when the cause of action, loss or harm truly occurred, giving rise to an insurance claim. The concept of a ‘retroactive date’ plays a decisive role in this framework.

In essence, a policyholder's retroactive date refers to the date that they first obtained or incepted their insurance policy. This is essentially the starting point from which insurers will consider any claims made; the birth of your insurance lifespan or what we also like to call, a peg in the sand where the proverbial clock starts ticking. It acts as a milestone date, marking the beginning of the insured individual's insurance lifespan.

In a claims-made scenario, the potential implications are that it means that there will be no coverage for any claims related to work performed in a professional capacity before the establishment of the retroactive date.

The intention is then for this retroactive date to continue with the policyholder throughout their insurance timeline or lifespan—even when switching to a new insurer that may be underwriting a new medical malpractice policy. Should an insured decide to transition between insurers, it is crucial that premiums are always paid and up to date, that there is absolutely no gap in cover and that the retroactive date is maintained, as once lost, it can never be reobtained. in essence should an insured wish to place a policy after losing their retroactive date, insurers will issue a new one, with a recent date, with all those years of coverage being lost.

Claims-made versus Occurrence-based coverage

When making the consideration of how the claims-made policies differ from occurrence-based, coverage, it is important to consider that it is the active policy at the time a claim is filed/notified that will be responsible for addressing the damages—as opposed to the policy in force during the incident itself or when the loss occurs. In the case of a claims-made basis policy, a key consideration is that lapsed or unrenewed policies will not provide coverage for any filed claims/notifications.

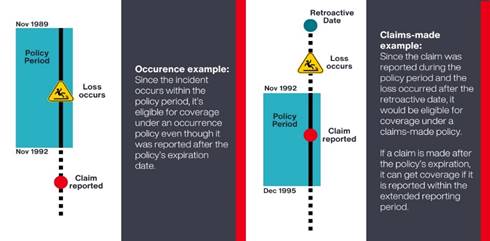

In order to truly understand how a retroactive date functions in medical malpractice coverage, consider this example[1]:

- A new occurrence-based medical malpractice policy is taken out on 1 November. 1989

- A client moves from occurrences cover to a claims made policy 1 November: 1992

- A claim was notified on 1 December 1995 for an incident that occurred in March of 1991

- The matter is stuck in litigation and an award for damages is issued on 1 December 2000. In this scenario, the occurrence-based policy will respond to the claim as the incident fell within the occurrence based policy lifespan.

- Any claims or matters that arise for work performed from 1 November 1992 will be covered by the claims made policy subject to the terms and conditions of the policy and on condition that the policy is active and maintained at the time the claim arises.

In a claims made scenario, the notification of circumstances are important in that even years later when a claim is made, the period under which the circumstance was notified will respond.

An in-depth understanding of the retroactive date is vital to understanding and assessing medical malpractice insurance policies. It seeks to provide clarity to both policyholders and insurers alike in determining coverage and in doing so it helps maintain a fair and transparent insurance solution for insurers.

The concepts of claims-made coverage for policyholders and a retroactive date in a medical malpractice insurance policy are closely linked to one another and in some cases may even create fear or uncertainty in the mind of a practitioner. However, by implementing prudent risk management strategies and promptly and timeously notifying the insurer about incidents or events, effective management of one’s matters or incidents will likely be achieved.

It is crucial to maintain continuous coverage so that you do not lose your retroactive date. While apprehensions regarding claims-made insurance coverage may exist, they can be addressed through conscientious risk management, timely and imminent notifications, well-organised practice management and a strong corporate governance structure.

The importance of expert advice from a specialist broker and well-informed risk manager that has deep expertise in medical malpractice cover is invaluable in helping you to understand your business's unique requirements and needs and find suitable risk management and insurance solutions. The contents hereof should not be construed as insurance broking advice and are of a general nature and as such, should not be used as a substitute for consultation with an insurance broker.

-- ENDS --

About Aon

Aon plc (NYSE: AON) exists to shape decisions for the better — to protect and enrich the lives of people around the world. Our colleagues provide our clients in over 120 countries and sovereignties with advice and solutions that give them the clarity and confidence to make better decisions to protect and grow their business. Aon South Africa (Pty) Ltd (an authorised financial services provider FSP 20555)

Follow Aon on LinkedIn, Twitter, Facebook and Instagram. Stay up-to-date by visiting the Aon Newsroom and sign up for News Alerts here.

Get new press articles by email

We submit and automate press releases distribution for a range of clients. Our platform brings in automation to 5 social media platforms with engaging hashtags. Our new platform The Pulse, allows premium PR Agencies to have access to our newsletter subscribers.

Latest from

- Yethu City Named Platinum Affordable Multi Family Residential Project Of The Year

- Eskom Becomes Foundation Customer At Proposed Zululand Energy Terminal For LNG Infrastructure

- Absa Force For Good Raises R3m For Good Morning Angels After Sun City Event

- BMW IT Hub Becomes Largest BMW Tech Centre Outside Germany Employing Over 2 500 Professionals

- Stigter Se Grootste Hindernis Is Leierskap Nie Marklimiete Nie

- LeadUP Podcast Season 6 Opens With Christopher Williams On Building CJ Distribution From Pharmacy Roots

- Practical Travel and Timing Tips for South African Firms Visiting Singapore for Regional Expansion

- JSE’s 2006 Self‑Listing Spurs Growth to R24.73tn Market Capitalisation

- Dubai Chambers Leads New Horizons Trade Mission To Johannesburg To Expand Bilateral Opportunities

- Vumela Invests in Breaze Delivery to Back Scalable Technology-Driven SME Growth

- AutoTrader Joins Jacaranda FM as Official Launch Partner for N1 Solar B Highway Billboard

- Limbada Emphasises Local Truths and Listening in New KFC India CMO Role

- Traderbag Launches Sustainable Paper Shopping Bags in Response to Unclear Recycling Labels

- KwaZulu‑Natal Department Flags Income Discrepancy in Illovu Housing Project Beneficiary Registration

- TFG Africa Sees 49.2% Online Sales Growth Driven By Bash Platform

The Pulse Latest Articles

- The Hidden Cost Of Living Crisis Is No Longer Inflation - It Is Energy (June 4, 2026)

- Hisense Powers Up For Fifa World Cup 2026 With New Tv Launch (June 4, 2026)

- Finfind Partners With The Silulo Foundation To Expand Funding Access For Underserved Msmes (June 2, 2026)

- You Can’t Measure What You Can’t Define – Or Can You? (part 3 Of 5) (June 2, 2026)

- South African Women Are Missing This Essential Nutrient (May 20, 2026)