Search results for: reliance

Exploring Nuclear Power and Wind Farms as Solutions to South Africa's Energy Problems

Germany is phasing out nuclear energy, France is stopping the expansion of wind energy, relying almost entirely on its nuclear fleet. South Africa, on the other hand, can use both to reduce the proportion of fossil-based electricity generation and stabilize electricity grids.

Is South Africa now doing exactly what Germany should have done - installing a solid energy mix?

South Africa stands at a crossroads in its energy landscape, grappling with significant challenges while seeking sustainable solutions to meet its growing power demands. The country's energy sector faces issues such as unreliable power supply, heavy reliance on fossil fuels, and the urgent need to reduce greenhouse gas emissions. In this context, the debate over nuclear power and the expansion of wind farms emerges as a critical discussion in addressing South Africa's energy crisis.

Energy Challenges in South Africa:

South Africa's energy challenges are multifaceted and complex, with repercussions across economic, social, and environmental domains. The reliance on coal for electricity generation has led to high emissions of greenhouse gases, contributing to climate change and air pollution. Furthermore, the country's power utility has struggled to maintain a stable power supply, resulting in frequent blackouts and load shedding that disrupt businesses and daily life.

Nuclear Power as a Controversial Option:

The discussion around nuclear power in South Africa is both complex and contentious. Proponents argue that nuclear energy can provide a stable and reliable base load power supply without the carbon emissions associated with fossil fuels. They highlight the potential for nuclear power to diversify the energy mix and reduce dependency on coal, contributing to long-term sustainability goals.

However, nuclear power also raises concerns, including safety risks, high initial costs, complex waste management, and public perceptions regarding nuclear accidents. The construction and operation of nuclear power plants require substantial investments and stringent regulatory oversight to ensure safety and environmental protection.

Nevertheless, nuclear energy is the safest form of energy production, especially when you consider that coal-fired power plants are themselves radioactive due to the "heavy" uranium content of hard coal!

The questionable German nuclear phase-out

It is strange that an energy-intensive industrial country like Germany has completely abandoned nuclear energy, while "nuclear" is booming all over the world. There are currently 422 reactors operating worldwide, two in South Africa with further reactors planned, and 57 are under construction all around the world.

Wind Farms: A Renewable Solution:

On the other hand, renewable energy sources like wind power offer a compelling alternative to fossil fuels and nuclear energy. South Africa boasts significant wind energy potential, particularly in regions like the Western Cape and Eastern Cape. Wind farms harness the natural power of the wind to generate electricity, providing a clean and renewable energy source.

Wind farms offer several advantages, including:

- Clean Energy: Wind power generates electricity without producing greenhouse gas emissions or air pollutants, contributing to a cleaner environment and mitigating climate change.

- Resource Abundance: South Africa has vast wind resources that can be harnessed for energy production, reducing reliance on finite fossil fuel reserves.

- Job Creation and Economic Growth: The development of wind farms stimulates economic activity, creating jobs in construction, maintenance, and related industries.

- Scalability and Modularity: Wind farms can range from small-scale community projects to large utility-scale installations, offering flexibility in meeting diverse energy needs.

Integrated Approach and Sustainable Transition:

A holistic approach to South Africa's energy transition involves integrating various energy sources to create a balanced and resilient energy mix. While nuclear power and wind farms represent distinct pathways, they can complement each other within a diversified energy portfolio.

Key considerations for a sustainable energy strategy include:

- Investment in Renewable Energy: Accelerating the deployment of wind farms and other renewables requires investment incentives, supportive policies, and streamlined regulatory processes.

- Nuclear Safety and Transparency: If pursuing nuclear power, a focus on safety standards, transparent decision-making, and public engagement is essential to build trust and ensure responsible nuclear energy development.

- Energy Efficiency and Demand-Side Management: Promoting energy efficiency measures and demand-side management practices can reduce overall energy consumption and optimize resource utilization.

- Research and Innovation: Continued research and innovation in energy technologies, grid integration, and storage solutions are crucial for advancing the transition to a sustainable energy future.

In conclusion, South Africa faces significant energy challenges that demand strategic planning, collaboration, and innovative solutions. While nuclear power and wind farms represent contrasting options, both can play a role in diversifying the energy mix and driving towards a cleaner, more resilient energy system. The path forward requires careful consideration of economic, environmental, and social factors to ensure energy security and sustainability for generations to come.

Every nut, bolt, and screw - forgings for harsh environments

The author is CEO of a small but highly certified German drop forge, supplying forgings for all kinds of energy systems: from coal and gas fired "fossil" plants over modern nuclear and solar thermal plants to wind turbines. He is regularly writing popular scientific articles about steel and its varied applications.

https://kb-schmiedetechnik.de/products.html

Examples are brackets, holders, hoists, hooks, mountings, chain links, special screws, pipe connections, pressure-bearing parts, valves, pieces for boiler systems and nuclear power plants, special vehicles such as agricultural machines, also parts and components for corrosive applications like naval architecture, ships, boats, seawater-suitable, corrosion-resistant components, acid-resistant, highly corrosion-resistant forgings for seawater applications, desalination, petrochemicals, fertilizer industry and production, food technology, drill equipment, oil rigs, marine technology, defense.

How artificial intelligence is re-shaping international arbitration practice

By Chandni Gopal, Partner, Prianka Soni, Senior Associate & Amaarah Mayet, Associate, Webber Wentzel

As the "great disruptor" of our time, artificial intelligence (AI), with its inherent ability to perceive, reason and solve problems, has enormous capacity to shape international arbitration practice.

The use of AI to enhance technological efficiency has long been accepted by the international arbitration community. In recent times, AI has emerged as a useful instrument that, when applied properly, can both increase the acceptance of international arbitration as the preferred forum for resolving commercial dispute resolution.

Current uses of AI

In international arbitration, the use of stenographers, short-hand techniques and backup audio recordings for the manual transcription of proceedings are not-too-distant memories. The need for time, resource and cost efficiencies propelled rapid technical breakthroughs that encouraged investment in machine learning and natural language processing (NLP) AI technologies. A direct offspring of these early technologies, voice-to-text technology, revolutionised transcription services, resulting in improved accuracy in record time, at a fraction of the cost.

It did not take long for machine learning, NLP and generative AI to be deployed in making document-intensive stages of the arbitration process considerably more efficient. Electronic discovery programmes, for example, can analyse huge amounts of electronically stored information, identify relevant material, and automatically collate them for discovery in a matter of hours (instead of days). In the discovery context, multilingual document review and translation software can offer initial content interpretation without the need for human linguists.

The international arbitration community has demonstrated sophistication in its receptiveness to new technologies while acknowledging the importance of appropriate checks and balances in protecting the integrity of the arbitration process. Translation software, for instance, may assist parties in identifying potentially relevant material despite it being in another language, but procedural rules generally afford the tribunal the discretion to direct the manner and form of translating documents for reliance purposes.

The international arbitration community has undoubtedly opened up a world of possibilities with both exciting prospects and challenging situations due to its controlled approach to AI-powered technologies.

Potential uses of AI

By harnessing AI technologies, arbitrators and legal practitioners can streamline the case management process. Firstly, AI can automate tedious tasks like analysing vast amounts of documents. Contracts, legal precedents, and evidence can be scanned in a fraction of the time it takes humans, allowing legal professionals to redirect their focus. Instead of sifting through mountains of paper, they can concentrate on building strong legal arguments and crafting persuasive submissions for their clients.

AI can also predict potential outcomes or suggest optimal dispute resolution strategies. By analysing past arbitration awards, relevant legal decisions, and arbitrator track records, AI algorithms can empower parties involved, including third-party funders, to make informed settlement decisions and the likelihood of claim success.

Witness preparation can also be streamlined with the help of AI-powered tools. These tools can analyse case documents, transcripts, arbitrator awards, and legal precedents to identify key issues and themes. This allows legal teams to create clear and persuasive submissions, develop tailored questioning strategies, highlight potential strengths and weaknesses in witness testimony, and ensure consistency in the narrative presented during hearings. Furthermore, AI can simulate cross-examination scenarios, helping witnesses anticipate tough questions and prepare effective responses.

Arbitrators themselves can benefit from AI's supportive capabilities. Machine learning AI can offer valuable assistance by creating preliminary timetables based on procedural rules, evidence rules, and party availability. AI can also assist with drafting routine sections of awards, such as factual backgrounds and historical context. By automating repetitive tasks, AI frees up arbitrators' time to focus on complex legal analysis and decision-making. Additionally, AI algorithms can play a vital role in quality control. By comparing language patterns, legal reasoning, and factual assertions in draft awards against established precedents and party submissions, AI can flag inconsistencies, factual errors, or potential biases. This not only enhances the quality and reliability of awards but also safeguards the integrity and fairness of the entire arbitration process.

The concept of a fully automated AI arbitrator remains a topic of debate. Concerns about AI hallucinations and biased reasoning are well-founded. However, AI's supportive capabilities offer intriguing possibilities. In cases with standardised contracts, clearly defined decision-making frameworks, or settled legal principles, AI arbitrators could expedite proceedings, reduce costs, and deliver more predictable outcomes. Even with the potential benefits, concerns about transparency, fairness, and adherence to the rule of law must be carefully addressed to ensure the legitimacy and acceptance of AI-driven international arbitration.

Responsibly Embracing Change

In essence, AI's role in arbitration goes beyond mere efficiency gains. It has the potential to fundamentally transform the nature of dispute resolution by augmenting arbitrators' capabilities, enhancing decision quality, and reshaping the dynamics of legal proceedings.

As AI becomes more sophisticated and integrated into the legal profession, stakeholders must navigate the complexities and opportunities presented by this paradigm shift. The rapid development of AI technologies underscores the urgency for the international arbitration community to adapt responsibly. This includes complying with new regulations and guidelines are ensuring professionals are properly trained.

The Silicon Valley Arbitration and Mediation Center, for example, has already released draft Guidelines on the Use of Artificial Intelligence (AI) in International Arbitration for Public Consultation (SVAMC Guidelines). The Guidelines place an emphasis on understanding AI’s limitations and risks, safeguarding the confidentiality, ensuring competent and diligent use of AI (including appropriate disclosure of its use), and ensuring that arbitrators do not delegate their decision-making responsibilities. The SVAMC Guidelines indicate that AI is becoming more involved in arbitration, and they serve as a useful reference guide for using AI's potential in arbitration safely and responsibly. International arbitration institutions are likely to follow suit by releasing their own guidelines in compliance with applicable laws and regulations.

The proliferation of AI regulation worldwide will also create peculiar challenges in the international arbitration community. AI technology used in international arbitration will need to remain compliant with new and differing regulations across various relevant jurisdictions. For instance, it is quite possible that different jurisdictions with different AI regulatory regimes house the laws governing the content of a dispute, the procedure of a dispute, and the venue at which the arbitration proceedings are held as agreed between the parties in the arbitration clause and agreement. In addition, it is important to the enforceability of the arbitral award that the award is rooted in the mandatory laws of the place where the award is rendered and the place where the enforcement of the award is sought.

These challenges also present an opportunity for international arbitration. When there are differences and conflicts in applicable laws, it creates an opportunity for practitioners to be creative. Thus creativity could lead to the harmonisation of various laws, or contribute to the development of flexible AI systems which are compliant and fit for purpose.

Overall, the use of AI in international arbitration requires a change-positive approach characterised by agility, adaptability and flexibility, as well as principled decision-making in which the rule of law, underlying purpose and legitimacy of international arbitration are safeguarded.

Africa Data Centres and DPA Southern Africa (SA) breaks ground on solar farm in Free State

The objective of the Free State farm is to furnish renewable energy to Africa Data Centres sites, commencing with its cutting-edge, carrier-neutral data centre in Cape Town, the CPT1 facility

JOHANNESBURG, South Africa, April 10, 2024/ -- Africa Data Centres and DPA SA (https://DPA-SA.co.za/) have broken ground on their solar farm in the Free State; The first phase will see power getting wheeled to its CPT1 facility; The second phase will see power being supplied to JHB1 and JHB2 once wheeling agreements with relevant municipalities conclude.

Africa Data Centres, a business of the Cassava Technologies group, is pleased to announce that it has broken ground on the construction of a solar farm in the Free State in collaboration with DPA Southern Africa.

This announcement forms a crucial component of the 20-year Power Purchase Agreement (PPA) inked in March 2023 with DPA Southern Africa a joint company of the French utility, EDF. The objective of the Free State farm is to furnish renewable energy to Africa Data Centres sites, commencing with its cutting-edge, carrier-neutral data centre in Cape Town, the CPT1 facility.

According to Cassava Technologies' President and Group CEO, Hardy Pemhiwa, “This initiative positions Africa Data Centres as a trailblaser in the data centre industry in responding to South Africa’s energy crisis through sustainable technology solutions. This is in line with a broader industry shift towards innovative, eco-friendly practices. The strategic use of solar power showcases technology's role in pioneering solutions for energy challenges and environmental sustainability”.

Furthermore, Tesh Durvasula, CEO of Africa Data Centres, underscores the commitment to powering all data centres with clean, renewable energy sources. "Today's announcement represents a significant stride in our initiative to energise South African data centres sustainably, advancing our objective of achieving carbon neutrality. The first phase involves constructing the 12MW solar infrastructure to power our Cape Town data centre, with subsequent phases extending to our Johannesburg data centres.”

Nawfal El Fadil, the CEO of DPA SA, states, "Africa Data Centres, as a pioneer in the data centre industry, has consistently demonstrated a strong commitment to sustainability, aligning seamlessly with our company's values. We are thrilled and honoured to contribute to Africa Data Centres’ mission of achieving carbon neutrality, beginning with the establishment of this solar power plant in the Free State to serve their data centre in Cape Town. At the heart of our collaboration lies a shared understanding that the path to carbon neutrality extends beyond infrastructure—it demands innovation, expertise, and collective determination to overcome challenges. DPA SA, backed by EDF's legacy, brings a wealth of experience and a proven track record in delivering high-quality, sustainable energy solutions to this partnership."

"We take immense pride in supporting Africa Data Centres on this journey, being among the pioneers in launching a wheeling solar plant, thereby paving the way for a greener, more sustainable future in South Africa," adds Nawfal El Fadil.

This project is a key element of Africa Data Centres' ambitious plans to emerge as the most sustainable colocation provider on the continent. "Beyond procuring renewable energy, our commitment to an efficiency strategy has earned us the internationally recognised ISO50001 certification for the effective operation of our data centres," Durvasula elaborates.

"Data centres worldwide face scrutiny for their reliance on grid power and renewables, and Africa is no exception. Africa Data Centres is actively addressing this issue by generating renewable energy, alleviating strain on the local grid. Additionally, our sustainability objectives encompass achieving net-zero status at all facilities, making this project another significant stride towards reaching that goal," concludes Durvasula.

Distributed by APO Group on behalf of DPA Southern Africa.

Follow Africa Data Centres on:

Twitter: https://apo-opa.co/4cKzd4r

LinkedIn: https://apo-opa.co/446fpol

Facebook: https://apo-opa.co/3TSkVGa

YouTube: https://apo-opa.co/3NcwWnp

About Africa Data Centres:

Africa Data Centres is your trusted partner for rapid and secure data centre services and interconnections across the African continent.

Africa Data Centres is Africa's largest network of interconnected, carrier and cloud-neutral data centre facilities. Bringing international experts to the pan-African market. We are your trusted partner for rapid and secure data centre services and interconnections across the African continent. Strategically located, our world-class facilities provide a home for all your business-critical data. Proudly African, we are dedicated to being the heart that beats your business.

Africa Data Centres' aim is to unveil various business opportunities and to develop a strategic network of partnerships. This will further strengthen Africa Data Centres' superiority in providing our customers with the highest standard of interconnected, carrier and cloud-neutral data centre facilities throughout Africa. www.AfricaDataCentres.com/

About Cassava Technologies:

Cassava Technologies is a technology leader providing a vertically integrated ecosystem of digital services and infrastructure enabling digital transformation. Launched in 2021, the company was born out of a need to create a digitally connected future that leaves no African behind. Through its subsidiaries, namely, Liquid Intelligent Technologies, Liquid Dataport, Liquid C2, Africa Data Centres, Distributed Power Africa, Sasai Fintech and Telrad, Cassava is a multinational technology company that has operations across key growth markets like Africa, the Middle East, Latin America and the United States of America. Cassava provides its customers in 94 countries with offerings that will help them grow, transform, and expand their operations. https://apo-opa.co/3U7rdmB

About DPA Southern Africa

DPA Southern Africa, a joint company of the French utility EDF and Distributed Power Africa, is at the forefront of the Southern African renewable energy market for businesses, laying the foundation for a sustainable and environmentally conscious future in South Africa and beyond.

Our commitment is to assist companies in achieving carbon neutrality and cost savings simultaneously by providing tailor-made renewable energy solutions that meet the specific needs of businesses. Our comprehensive offerings include on-site, wheeling, and storage solutions, offering businesses a holistic approach to sustainable energy management.

SOURCE: DPA Southern Africa

Transforming Home Comfort: The New Age of Smart Blinds and Light Switches

In the constantly evolving world of smart home technology, two innovations have significantly changed how we interact with our living spaces: smart blinds and smart light switches. These advancements are not just about embracing modernity; they are about enhancing convenience, energy efficiency, and personalising home environments to suit our lifestyles. Let’s delve into how these smart home features are redefining comfort and convenience in our daily lives.

Smart Blinds: Redefining Window Treatments

Smart blinds are a groundbreaking innovation in home automation. These are not your average window coverings; smart blinds offer unparalleled convenience and control over your home’s natural lighting and privacy. With smart blinds, you can adjust the amount of light entering your home with just a tap on your smartphone or through voice commands via smart home assistants like Amazon Alexa or Google Home.

The Convenience Factor

Imagine waking up to gently rising blinds that sync with your alarm, letting in that soft morning light. Or picture adjusting your blinds to close automatically as the sun sets, all without moving an inch from your couch. This level of convenience is not a luxury anymore; it’s a reality with smart blinds.

Energy Efficiency

Smart blinds also contribute significantly to energy efficiency. They can be programmed to open or close based on the time of day, temperature, or even the position of the sun. This automation helps in maintaining a consistent temperature in your home, reducing the reliance on heating and cooling systems, and thus saving on energy bills.

Smart Light Switches: Lighting at Your Fingertips

Moving on from natural light management to artificial lighting, smart light switches are the next big thing in home automation. They replace traditional light switches and offer an enhanced, interactive experience.

Enhanced Control and Customization

With smart light switches, you can control the lighting in your home from anywhere. Whether you’re in bed and forgot to turn off the kitchen lights or away on vacation and want to switch lights on and off periodically for security, smart switches make it possible. They also allow you to create custom lighting scenes for different activities or moods, adding a whole new dimension to your home’s ambiance.

Integration with Home Automation Systems

One of the most significant advantages of smart light switches is their ability to integrate seamlessly with other smart home devices. This integration enables you to create a cohesive, fully automated smart home system. You can program your lights to turn on as your smart blinds open, syncing your home’s lighting with natural light patterns for a more natural wake-up routine.

Conclusion: Embracing a Smarter, More Comfortable Home

In conclusion, smart blinds and smart light switches are not just gadgets; they are essential components of a modern, efficient, and comfortable home. They offer convenience, energy savings, and an enhanced living experience. As we continue to embrace smart home technology, these innovations represent a step towards a future where our homes are not just places we live in but are dynamically integrated into our lifestyles, responding to our needs and preferences seamlessly. The future is smart, and it’s here to make our lives more comfortable and our homes more enjoyable.

Fostering Resilience In Young Children Is Vital To Their Healthy Development

How do we do this?

Nurturing resilience in young children is paramount for their growth and development in a country and world filled with challenges. Ursula Assis, Country Director of Dibber International Preschools, sheds light on this crucial aspect of parenting, teaching, and early childhood education and development.

As Assis explains, resilience refers to a child's ability to respond positively to adverse events. While some may perceive resilience as an innate trait, she stresses that it can also be cultivated through cognitive, emotional, and social skills. "Resilience is not just about bouncing back from setbacks; it's also about equipping children with the tools to navigate life's uncertainties with confidence and adaptability," says Assis.

Here are nine practical ways parents can foster resilience in their young children, according to Assis:

Setting Boundaries: Assis advises parents to set boundaries and encourage independence in their children. Saying 'no' when appropriate and allowing children to tackle tasks independently instils a sense of self-reliance and responsibility.

Avoiding Overprotection: While ensuring safety is essential, she cautions against overprotecting children. Allowing them to explore, experiment, and occasionally experience failure is crucial for their growth and resilience.

Building Strong Family Bonds: A supportive and loving family environment lays the foundation for resilience. Spending quality time together, fostering open communication, and nurturing emotional stability contribute to a child's ability to cope with challenges.

Asking Empowering Questions: Assis suggests asking 'how' questions to encourage problem-solving skills and a positive outlook instead of focusing on mistakes. This approach helps children develop resilience by shifting their perspective from dwelling on failures to finding solutions.

Embracing Mistakes: Making mistakes is a natural part of learning and development. Assis advocates for allowing children to make and learn from mistakes, emphasising that resilience is built through overcoming challenges.

Encouraging Healthy Risk-Taking: It is key to highlight the importance of encouraging children to take calculated risks and step out of their comfort zones. Providing guidance on assessing risks and taking appropriate precautions empowers children to explore new opportunities confidently.

Storytelling and Inspiration: Sharing stories of resilience and perseverance inspires children to believe in their own abilities. Assis recommends storytelling as a powerful tool for instilling values of determination, passion, and resilience in young minds.

Positive Communication: The tone of communication plays a significant role in shaping children's perceptions and responses to challenges, with parents encouraged to communicate positively and emphasising encouragement and support rather than fear or negativity.

Providing Unconditional Support: While fostering independence, the importance of maintaining a supportive presence in children's lives needs to be stressed. Knowing they have a reliable source of love and guidance gives children the confidence to navigate obstacles and seek help when needed.

In conclusion, Assis reiterates that parents play a crucial role in modelling resilient behaviour for their children. By incorporating these strategies into parenting practices, parents can empower their children to thrive in the face of adversity. Dibber International Preschools is dedicated to supporting parents in this journey of fostering resilience and nurturing the next generation of confident, resilient individuals.

Moving SA point-of-sale into a smarter future

The digitalisation of the modern world economy is being driven rapidly by a shift from traditional payment methods. Fatima Khota, Business Unit Manager in Rectron’s Point-of-Sale (POS) Division looks at how retailers in the formal and informal sector are adopting smart innovations to better serve customers anywhere in the world, in-store or on the streets.

According to recent studies, the global point-of-sale (POS) market is projected to almost quadruple between 2023 and 2030, from $25,28billion to $81,15billion.

The Middle East is set to grow at a compound annual growth rate (CAGR) of 16,8% in that time, with South Africa expected to experience a CAGR of 9,9% between 2022 and 2028.

Non-traditional money

The World Economic Forum reports that only 48% of Africa’s population has access to traditional banking services, like bank accounts or credit cards.

This has led to the emergence of creative payment solutions, like mobile money, digital wallets, gift cards and other options that don’t require a bank account, including cryptocurrencies.

No longer do entrepreneurs (many being one-person operations) need expensive traditional POS devices to trade in a cashless way but can use their smart mobile phones or tablets to enjoy the same functionality, at a fraction of the cost.

Even people with traditional accounts are adoption an array of new payment options, like Google Wallet, Apple Pay, Amazon Pay, PayPal, Venmo, CashApp, and other apps and services.

Credit cards complete with buy-now-pay-later (BNPL) services are growing rapidly, with financial service providers allowing consumers to make purchases and pay in instalments, often with no interest.

The power of AI

In-store, retailers are leveraging the power of big data and analytics to create a more personalised experience for customers through their POS capabilities.

For instance, artificial intelligence allows businesses to offer customised recommendations and promotions at checkout, based on customer histories.

Furthermore, over time, tracking tools can offer deeper insights into consumer preferences and seasonal trends, allowing for better stock keeping and wholesale buying.

In the United States, the world’s biggest retailer Walmart has taken POS to the next level, integrating it with other technologies to change and monitor consumer behaviour in-store, and improve the overall customer experience.

For instance, the retailer has adopted the use of infrared technology to track where people have gathered in-store, so that assistants can be dispatched to these areas to offer help.

Automated POS

Clearly, the days of a one-size-fits-all approach to point of sale are gone, as a variety of mobile devices, cloud-based POS, acceptance of cryptocurrencies and even self-service check-out is set to drive efficiencies and substantially lower costs.

With increased automation already making its way into South African retail environments, notably in fast-food restaurants and even in stock rooms (robots), the impact on employment has to be considered and managed carefully.

Although some of these technologies will reduce the need for certain manual jobs (like tellers and stock counting), it be seen as a mechanism to streamlining activities and get to the areas where people cannot.

These innovations should not be seen as hampering employment, but rather as helping to transform the nature of work and even create new opportunities.

Automation helps free up time for employees to get more face time with customers, enhancing the services they offer through expert consultation and direct engagement.

Automation ought to help build greater efficiencies (and precision) into processes, keep workloads low, productivity (as well as profitability) high. This will in turn increase the demand for newer, more skilled job roles and opportunities.

Opportunities in POS

With better efficiency through automation of tasks, workers get more time to focus on value-added tasks. Quicker data processing and turnaround times serve to offer better and faster customer responses at every touchpoint.

Modern POS systems can store and receive data (for example from the on-premise stock room, as well as the national network of stores in real-time), which can be valuable when planning (using statistics to inform store buying decisions). Inventory control helps maintain stock levels and manages more accurate stock profiles.

Opportunities for upselling and cross-selling can add onto existing POS solutions, while improving security (systems reduce the reliance on cash transactions and protect consumer accounts better).

As South African POS technology evolves, shaped by the country’s unique formal and informal retail landscape, employees, business owners and consumers alike are set to enjoy better value-for-money, as well as a much more fulfilling trade and shopping experience.

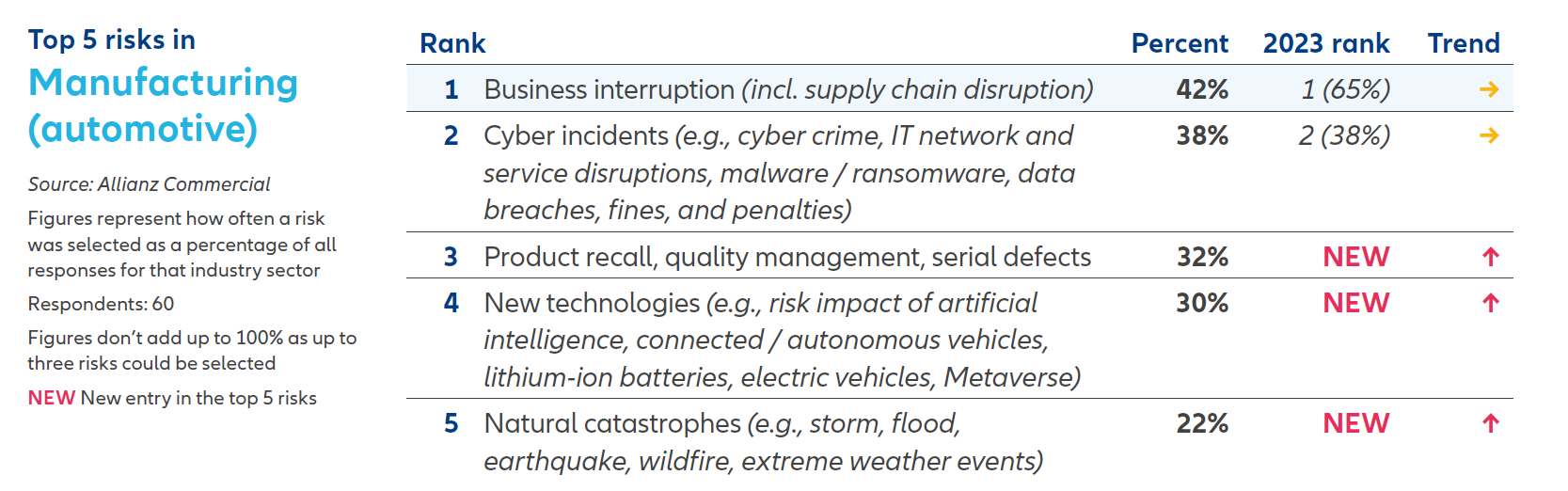

Business interruption and Cyber concerns top risks for automotive manufacturing sector in 2024, Allianz Risk Barometer reveals

- Business interruption ranks #1 with 42% of responses.

- Data breaches, attacks on critical infrastructure or physical assets and increased ransomware attacks drive cyber concerns to #2 with 38% of responses.

- Product recall, quality management, serial defects features as a new risk in #3 with 32% of responses.

Johannesburg, March 25, 2024 – Business interruption and cyber incidents are the primary concerns for the manufacturing sector within the automotive industry in 2024, according to the Allianz Risk Barometer. The report, based on insights from over 3,000 risk management professionals and business leaders, highlights the growing importance of addressing these risks to ensure business continuity and safeguard against potential disruptions.

Despite a slight easing of post-pandemic supply chain disruption in 2023, Business interruption continues to hold its position as the number one threat for automotive manufacturing, with 42% of respondents expressing concern. Cyber incidents and natural catastrophes are the top two causes of business interruption feared most by companies, followed by fire and machinery/equipment breakdown or failure. These results underscore the interconnectedness and volatility of the global business environment, as well as the reliance on supply chains for critical products or services. Consequently, improving business continuity management, identifying supply chain bottlenecks, and developing alternative suppliers remain key risk management priorities for companies in 2024.

The COVID-19 pandemic and its subsequent disruption to supply chains have served as a wake-up call for companies. Compared to pre-pandemic times, businesses are now better prepared for business interruption or supply chain events. According to the Allianz Risk Barometer, the most common actions taken to de-risk supply chains include developing alternative suppliers (60% of responses), improving business continuity management (42%), and identifying and remediating supply chain bottlenecks (37%).

According to the Allianz Trade’s Automotive sector risk report, the automotive market is expected to normalize this year as demand loses momentum following a strong rebound in 2023. The growth of new auto registrations is expected to slow down to +1.9%. New auto registrations saw a significant recovery in 2023 as Covid-induced supply-chain disruptions eased, and pent-up demand released. Additionally, resilient economic growth and strong, albeit slowing, growth in EVs fuelled car sales - total global auto registrations increased by +11.3% to nearly 88mn, though is still below pre-pandemic levels.

For the second consecutive year, Cyber incidents rank as the second most important risk in automotive manufacturing, with 38% of respondents expressing concern. The recent surge in ransomware attacks saw insurance claims activity increase by over 50% compared to 2022. Hackers are increasingly targeting IT and physical supply chains, launching mass cyber-attacks, and finding new ways to extort money from businesses. As a result, early detection and response capabilities and tools are becoming increasingly crucial. Investment in detection backed by artificial intelligence is expected to enhance incident identification. Without effective early detection tools, companies may experience longer unplanned downtime, increased costs, and a greater impact on customers, revenue, and reputation.

“Cyber criminals are exploring ways to use new technologies such as generative artificial intelligence (AI) to automate and accelerate attacks, creating more effective malware and phishing. The growing number of incidents caused by poor cyber security, in mobile devices in particular, a shortage of millions of cyber security professionals, and the threat facing smaller companies because of their reliance on IT outsourcing are also expected to drive cyber activity in 2024, “explains Santho Mohapeloa, Cyber Insurance Expert, Allianz Commercial.

Product recall, quality management, and serial defects emerge as a new risk at #3 with 32% of respondents identifying it as a concern. The automotive sector bears the brunt of product recall losses, accounting for over 70% of the value of all losses. The increasing complexity of supply chains and stricter regulations contribute to the rising impact of product recalls on companies' financials and reputations. With recalls affecting a higher number of units, driven by factors such as faster speed-to-market and outsourcing of research and development, the automotive sector remains a frequent driver of claims.

As the automotive manufacturing sector faces these risks head-on, companies must prioritize risk management strategies and enhance their resilience. By proactively addressing Business interruption, Cyber incidents, and Product recall risks, companies can safeguard their operations, reputation, and bottom line.

View the Allianz Risk Barometer methodology and full global and country risk rankings

About the Allianz Risk Barometer

The Allianz Risk Barometer is an annual business risk ranking compiled by Allianz Group’s corporate insurer Allianz Commercial, together with other Allianz entities. It incorporates the views of 3,069 risk management experts in 92 countries and territories including CEOs, risk managers, brokers and insurance experts and is being published for the 13th time.

-- ENDS --

For further information please contact:

Johannesburg: Lesiba Sethoga

Tel. +27 112 147 948

This email address is being protected from spambots. You need JavaScript enabled to view it.

About Allianz Commercial

Allianz Commercial is the center of expertise and global line of Allianz Group for insuring mid-sized businesses, large enterprises and specialist risks. Among our customers are the world’s largest consumer brands, financial institutions and industry players, the global aviation and shipping industry as well as family-owned and medium enterprises which are the backbone of the economy. We also cover unique risks such as offshore wind parks, infrastructure projects or Hollywood film productions. Powered by the employees, financial strength, and network of the world’s #1 insurance brand, as ranked by Interbrand, we work together to help our customers prepare for what’s ahead: They trust us to provide a wide range of traditional and alternative risk transfer solutions, outstanding risk consulting and Multinational services, as well as seamless claims handling. The trade name Allianz Commercial brings together the large corporate insurance business of Allianz Global Corporate & Specialty (AGCS) and the commercial insurance business of national Allianz Property & Casualty entities serving mid-sized companies. We are present in over 200 countries and territories either through our own teams or the Allianz Group network and partners. In 2022, the integrated business of Allianz Commercial generated more than €19 billion gross premium globally.

These assessments are, as always, subject to the disclaimer provided below.

Cautionary note regarding forward-looking statements

This document includes forward-looking statements, such as prospects or expectations, that are based on management's current views and assumptions and subject to known and unknown risks and uncertainties. Actual results, performance figures, or events may differ significantly from those expressed or implied in such forward-looking statements.

Deviations may arise due to changes in factors including, but not limited to, the following: (i) the general economic and competitive situation in Allianz’s core business and core markets, (ii) the performance of financial markets (in particular market volatility, liquidity, and credit events), (iii) adverse publicity, regulatory actions or litigation with respect to the Allianz Group, other well-known companies and the financial services industry generally, (iv) the frequency and severity of insured loss events, including those resulting from natural catastrophes, and the development of loss expenses, (v) mortality and morbidity levels and trends, (vi) persistency levels, (vii) the extent of credit defaults, (viii) interest rate levels, (ix) currency exchange rates, most notably the EUR/USD exchange rate, (x) changes in laws and regulations, including tax regulations, (xi) the impact of acquisitions including related integration issues and reorganization measures, and (xii) the general competitive conditions that, in each individual case, apply at a local, regional, national, and/or global level. Many of these changes can be exacerbated by terrorist activities.

No duty to update: Allianz assumes no obligation to update any information or forward-looking statement contained herein, save for any information we are required to disclose by law.

Privacy Note: Allianz Commercial is committed to protecting your personal data. Find out more in our privacy statement.

Tech2Desk: The Affordable Medical Aid Your PC Didn’t Know It Needed

In the digital age, where technology is intertwined with every facet of our lives, ensuring our computers are in optimal health is paramount. Enter Tech2Desk, the revolutionary service that’s fast becoming the medical aid for PCs, offering a comprehensive care package that keeps your technology not just running, but thriving.

Just as medical aid plans are designed to keep us healthy, prevent illness, and ensure access to treatment when we need it, Tech2Desk provides a similar safety net for our computers. With an ever-increasing reliance on technology for both personal and professional use, having a service that acts as a guardian for your PC’s wellbeing is more crucial than ever.

Preventive Measures and Immediate Care

Much like regular health check-ups, Tech2Desk offers preventive measures to ensure your computer’s longevity. Through regular maintenance, updates, and security checks, Tech2Desk works tirelessly to prevent issues before they arise, mirroring the preventive care we seek for our own health.

However, when problems do surface, Tech2Desk’s rapid response mimics that of emergency medical services, providing swift, expert care to diagnose and treat issues without the need for lengthy downtime. This immediate care is crucial in today’s fast-paced world, where even a small hiccup in our technology can lead to significant disruptions in our daily lives.

Inexpensive Fixed Monthly Fee with AI-Assisted Support

Tech2Desk’s approach to IT support is refreshingly simple and user-friendly. By eschewing the traditional models of hourly rates and long-term contracts, Tech2Desk offers its services for an inexpensive fixed monthly fee per PC. This model not only provides businesses and individuals with unlimited support for all their computer issues and needs but also ensures that there are no unexpected bills — much like a comprehensive medical aid plan where you know exactly what you’re covered for and can access services without fear of hidden costs.

Moreover, Tech2Desk’s support is bolstered by AI-assisted capabilities, enhancing the efficiency and effectiveness of the service. Through intelligent algorithms and machine learning, Tech2Desk is able to provide even faster issue resolution, proactive system monitoring, and predictive maintenance, ensuring that your PC stays in optimal health at all times.

Customized Care for Every Need

Understanding that every business and individual has unique needs, Tech2Desk’s team of specialist technicians works closely with clients to develop custom solutions. Whether it’s setting up a new network, troubleshooting software issues, or providing cybersecurity guidance, Tech2Desk tailors its services to meet each client’s specific requirements, much like a medical specialist would tailor treatment to a patient.

A Trusted Partner in Your PC’s Health

Tech2Desk’s commitment to excellence and customer satisfaction has made it a trusted partner for businesses of all sizes. Its innovative approach to IT support has saved its clients thousands of dollars in unexpected bills, highlighting the value of having a reliable ‘medical aid’ for your PC.

As technology continues to evolve and become even more integral to our daily lives, the importance of keeping our digital devices in top health cannot be overstated. Tech2Desk stands at the forefront of this movement, offering a comprehensive, worry-free service that ensures our PCs are always in peak condition, ready to support us in all our endeavors.

In conclusion, just as we invest in medical aid to safeguard our health, investing in a service like Tech2Desk is essential for anyone looking to protect and optimize their technological assets. Tech2Desk is not just a service; it’s peace of mind, ensuring that our digital lifelines are always in the best hands.

Print and its pride of place in education

The role of print in enhancing the education sector

Reports of matriculants battling to complete their final exams due to poor print quality of exam papers, is another clear indication of the education sector’s reliance on print.

While classroom learning, thanks to technology, has moved far beyond the era of overhead projectors and chalkboard dust, the role of print and paper will forever have its place in school learning.

This is a contentious statement for many, who believe that print is an outmoded way of producing and consuming learning materials, believing that e-learning is the only way learners will get ahead – especially in a digital era. In their 2019 annual letter, Bill and Melinda shared a similar sentiment saying that textbooks would soon be obsolete.

The South Africa reality however, paints a very different picture.

Screens have their limitations

There are advantages to digital learning compared to traditional textbook learning, including increased engagement. However, it's important to note that digital screens are not the only effective solution for educating our children. Several research studies have demonstrated that people tend to comprehend more from printed learning materials than their digital versions. This is because digital screens can cause distractions such as pop-ups, or easy access to social media and email, which can draw readers away from the main content. In contrast, when reading printed texts, readers can fully immerse themselves in the material, leading to a better understanding and retention.

We are all aware of the potential risks involved with allowing young children to spend too much time in front of screens for entertainment, while we try to get some work done or simply take a break. Excessive screen time can lead to eye strain and headaches and has also been linked to increased symptoms of attention deficit hyperactivity disorder (ADHD) in children. Moreover, blue light exposure caused by screens can disrupt also sleep patterns.

The digital divide

The integration of digital technology in schools has heightened the digital divide in South Africa. Almost 80% of students are unable to afford tablets and laptops to access educational materials. However, using print materials can create cost-effective and engaging learning experiences that are accessible to all learners, irrespective of their socioeconomic background.

“Print will always have pride of place in the education field, not only because access to the internet and digital resources limited for so many communities of learners in South Africa, but because print is an efficient, conducive medium for learning. You can read a book or complete a worksheet anywhere, but you are at the mercy of everything from connectivity access to battery life when relying on digital platforms for learning,” says Timothy Thomas, Epson South Africa Country Manager.

Creating the next generation of eco heroes

Epson believes that sustainability and technology must come together to drive social change. To demonstrate this principle, the company consistently develops products and initiatives that align with environmental objectives. With Epson Heat-Free printers, energy consumption is significantly reduced, compared with laser printers, and with the option of double-sided printing, paper wastage is instantly reduced.

Application for Leave to Appeal Default Judgment after Failed Rescission Applications

Msizi Mhlongo | SchoemanLaw Inc

Category: Civil Litigation and Alternative Dispute Resolution

Introduction

Can a default judgment that has been subject to rescission applications be appealed by a party?

In the matter of Road Accident Fund v Gonsalves (14756/2017) [2024] ZAGPJHC 130 (7 February 2024), Judgment by default was granted against the Road Accident Fund (“the RAF”) in May 2022. Almost a year after the judgment date, the RAF launched an application for leave to appeal the default judgment, and condonation for the late filing of the application.

The Appeal

The RAF sought only to appeal the loss of earnings award – by far the largest part of the quantum. Ms Gonsalves raised a point in limine that it was not open to RAF to appeal the judgment when it was still open to rescission, and the court requested submissions on the issue of appealability.

Condonation of Appeal

Justice Yacoob (“the Justice”) considered Ms Gonsalves’ contention regarding the condonation application that the delay was unreasonable, that the RAF’s defence had been struck out in October 2021, due to its non-compliance with the rules and applicable practice directives, and the RAF did not seek to have the order rescinded, and the RAF’s assertion in its affidavit in support of the condonation application that in February 2023 it was under the impression that an application for rescission was appropriate, but its applications for rescission had been unsuccessful.

Rescission

The Justice noted that the success or failure of other applications for rescission was irrelevant, that each rescission application was considered on its own merits, and that RAF did not disclose how many applications for rescission it had brought, and what the reasons for the failures were. She discussed Pitelli where the Supreme Court of Appeal held that an order is not final until the court of first instance is incapable of revisiting the order, and that since an order taken in the absence of one party is open to being revisited, it is ordinarily not appealable until an application for rescission has been unsuccessful.

The Justice considered the obiter dictum in Sparks, distinguished Moyana (relied on by the RAF), and considering RAF’s reliance on Mogorosi, she pointed out that the question at this stage was whether the order RAF sought to challenge, is at this stage final and therefore appealable – and that she was satisfied that it was not. She recorded that even if it were open to RAF as a litigant to change the status of the order by its own preference, by following the line of case law which begins with Sparks, there was no explicit waiver in the application for leave or in the affidavit filed in support of the application for condonation, and that she was doubtful that RAF could simply rely on the fact that it had brought an application for leave to ask the court to infer that it had waived a right to apply for rescission.

Effluxion of time

On the effluxion of time, the Justice pointed out that the RAF was as much out of time for an application for leave to appeal as it was for an application for rescission, and would have to obtain condonation either way, so that did not weigh on either side of the debate.

The Justice noted that there may be some circumstances where it was appropriate that an order that was still open to rescission should be appealable, but she did see that any such circumstances are present in casu. The application by the RAF was dismissed with costs.

Conclusion:

For parties subject to litigation, it is of paramount importance to ensure that you comply with the Rules, more especially when time limits are involved, in order to avoid matters being struck off the roll and incurring a costs order.

Msizi Mhlongo | SchoemanLaw Inc

Attorney

https://schoemanlaw.co.za/our-services/civil-litigation-and-alternative-dispute-resolution/